According to CoreLogic’s 2022 Mortgage Fraud Report, 1 in every 131 mortgage applications contains some indication of fraud. Income misrepresentation was identified as the most common type of application fraud. However, it’s important to note that misrepresentation of assets, occupancy, and other information also occur.

Unfortunately, some people may intentionally lie on their mortgage application in an attempt to improve their chances of getting approved or to secure better loan terms. Others may unintentionally provide inaccurate or incomplete information without realizing the potential consequences.

It’s important to understand that lying on a mortgage application is considered mortgage fraud, which is a serious offense that can result in criminal charges, fines, and even imprisonment. If a borrower is found to have lied on their mortgage application, their loan may be denied or their existing mortgage could be called due and payable immediately.

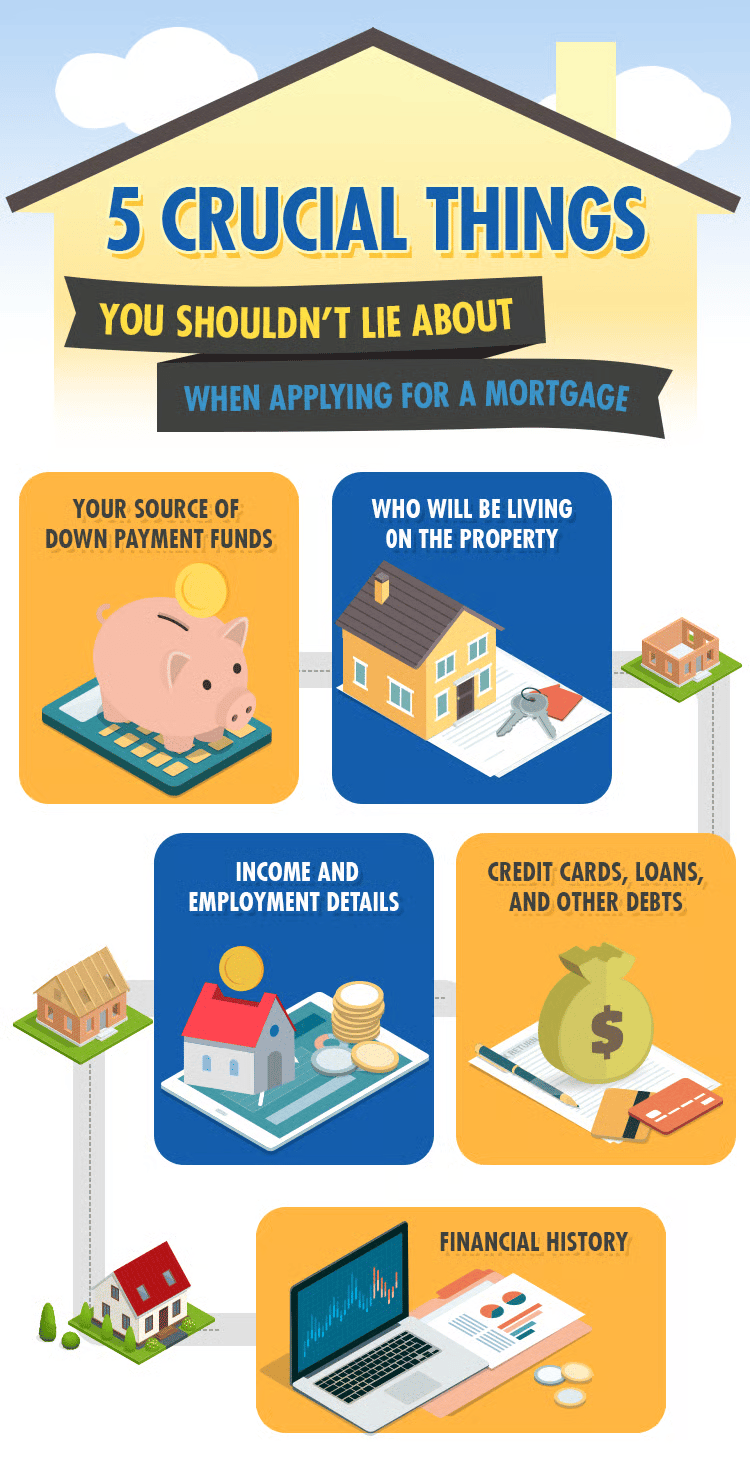

If you're planning to apply for a mortgage anytime soon, here are five crucial things you should never lie about:

1. Source of Your Down Payment Funds

When applying for a mortgage, lenders will ask where your down payment money is coming from to ensure that you have the financial means to make the payment and to verify that the funds are legitimate. If you're using a gift from a family member, for example, the lender may require a gift letter stating that the funds are a gift and not a loan that needs to be repaid.

Lying about the source of your down payment funds can lead to serious consequences, including loan denial or legal action. It’s always best to be honest and transparent with your lender about where your money is coming from.

2. Who Will Be Living in the Home

When applying for a mortgage, you’ll be asked whether the property will be your primary residence, a second home, or an investment property. Lenders use this information to determine the risk associated with the loan and to set interest rates accordingly.

Some borrowers may be tempted to lie and claim that they will be living in the home when they actually plan to rent it out. This is known as occupancy fraud and is considered a serious offense that can result in loan denial or legal action.

3. Your Income and Employment Status

When applying for a mortgage, lenders will ask for documentation of your income and employment status to determine your ability to repay the loan. Some borrowers may be tempted to exaggerate their income or misrepresent their employment status to qualify for a larger loan or better terms.

However, lenders will typically verify this information through pay stubs, tax returns, and employment verification. Lying about your income or employment status can result in loan denial or legal action, and may even lead to criminal charges in some cases.

4. Your Debts

When applying for a mortgage, lenders will ask for a list of your debts, including credit card balances, student loans, and other monthly payments. This information is used to calculate your debt-to-income ratio, which is an important factor in determining your ability to repay the loan.

Some borrowers may be tempted to leave out certain debts to improve their debt-to-income ratio, but this is considered fraud and can result in loan denial or legal action.

5. Your Financial History

When applying for a mortgage, lenders will review your credit report and financial history to assess your creditworthiness and ability to repay the loan. This includes information such as bankruptcies, foreclosures, and late payments.

Some borrowers may be tempted to omit or misrepresent this information in order to improve their chances of getting approved. However, lenders have access to a variety of tools and resources to verify your financial history, and any discrepancies can result in loan denial or legal action.

What Happens if You're Caught Lying on Your Mortgage Application?

If you're caught lying on your mortgage application, you could face serious consequences, including:

Your loan may be denied.

If you’ve already been approved, your loan may be called due and payable immediately.

You may be required to pay a higher interest rate or face other penalties.

You could face legal action or criminal charges for mortgage fraud.

Mortgage fraud is a serious offense that can result in fines of up to $1 million and up to 30 years in prison.

Bottom Line

Always be honest and transparent when applying for a mortgage. Lying on your application may seem like a harmless shortcut, but it can have serious and lasting consequences.

If you're unsure about how to answer a question on your application or need help navigating the mortgage process, don't hesitate to reach out to a trusted mortgage professional for guidance.