In simplest terms, a mortgage is a long-term loan designed to help borrowers purchase a house. It allows individuals to become homeowners without making a large down payment, thus fulfilling the American Dream.

Once you become a homeowner, a mortgage represents one of your life's biggest financial commitments. That’s why it’s important to understand the structure of your payments — what percentage goes to principal, interest, taxes, and what you currently owe on your loan balance.

I'm a First-Time Home Buyer. Once I Closed on My New Home, When Will My Mortgage Payment Start?

Mortgage payments usually start one full month after the last day of the month in which the home purchase closed.

Unlike rent payments, which are typically paid in advance on the first day of the month, mortgage payments are paid in arrears — meaning the payment is made at the end of the month.

Example: If you close on your new home on March 28, your first full mortgage payment (for April) is due May 1.

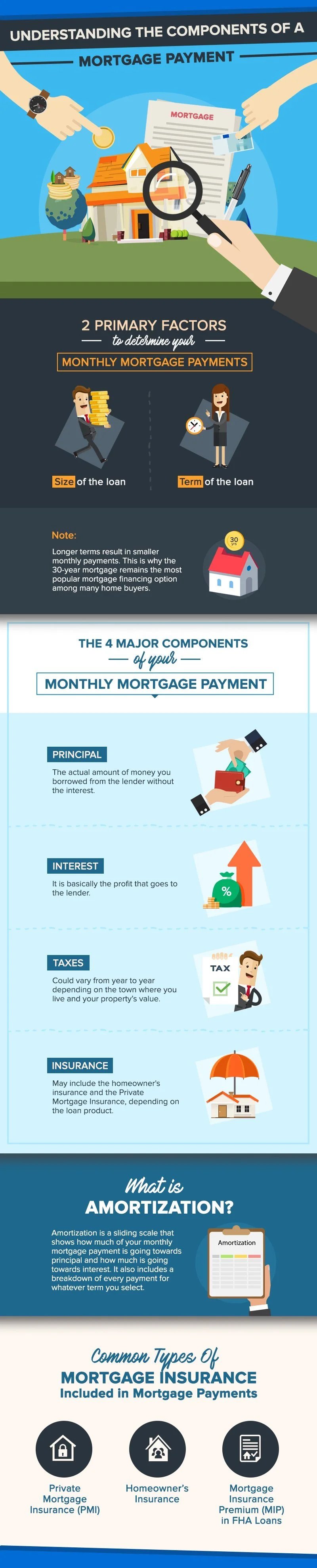

2 Primary Factors That Determine Your Monthly Mortgage Payments

-

Size of the loan – The amount of money borrowed.

-

Term of the loan – The length of time within which the loan must be fully repaid.

Remember: Longer terms result in smaller monthly payments. That’s why the 30-year mortgage remains the most popular financing option among many home buyers.

Remember PITI: The 4 Major Components of a Mortgage Payment

PRINCIPAL

The actual amount of money borrowed from the lender without interest — the face value of your mortgage on the first day.

Example: If your mortgage is $250,000 with a 4.5% interest rate, your principal starts at $250,000. A portion of each payment goes toward repaying this amount.

With a fixed-interest rate loan, your principal repayment amount stays the same for the life of the loan. However, more of your payment goes toward principal in the later years, since early payments are mostly applied to interest.

Formula:

Principal Balance = Purchase Price + Fees Rolled into Mortgage − Down Payment

INTEREST

The interest is the lender’s profit — their reward for taking the risk of lending money. Lenders collect most of their interest early in the loan term before the principal starts decreasing significantly.

For a 30-year loan, the first seven years are heavily interest-based, though each month a small portion still goes toward the principal.

Higher interest rates = higher mortgage payments

Interest accrues annually, whether you have a fixed-rate or adjustable-rate mortgage. The average 30-year fixed mortgage rate until March this year was 4.54%, slightly higher than November 2017.

Formula:

Interest Portion = Current Principal Balance × (APR ÷ 12)

Side Note: What is Amortization?

Amortization is a sliding scale showing how much of each monthly payment goes toward principal versus interest. It includes a breakdown for the entire term. You can request a copy from your lender or use free online amortization calculators to estimate your monthly payments.

TAXES

Most lenders require you to escrow property taxes into your monthly payment because taxes take priority over everything else.

Property taxes vary by location and property value. They fund public services such as schools, road construction, and police/fire departments.

If you escrow, your lender collects a portion each month and pays the tax bill for you. Any surplus at year’s end may be refunded or applied toward next year’s taxes.

INSURANCE

Like taxes, insurance is typically part of each monthly mortgage payment and held in escrow until the bill is due. This ensures you’re always covered in case of emergencies.

Insurance and tax costs usually remain steady unless affected by events like severe weather or shifts in foreclosure rates.

Common Types of Mortgage Insurance Included in Payments

Private Mortgage Insurance (PMI)

Required for borrowers with less than 20% down, PMI protects the lender if you default. Costs typically range from 0.3% to 1.15% of the loan amount and depend on factors like credit score and down payment.

For most conventional loans, PMI can be removed once you have at least 20% equity. Payment plans may be annual, monthly, or upfront.

Homeowner’s Insurance

A form of property insurance that covers losses and damages to your home and assets, and provides liability coverage for accidents on your property.

Mortgage Insurance Premium (MIP) in FHA Loans

MIP protects lenders from losses in FHA loans. Both upfront and annual premiums are required for all borrowers, regardless of down payment.

You can check current annual MIP rates on the FHA website.