Applying for a mortgage is not a walk in the park—especially when your credit score falls below 740, which lenders consider to be a “very good” score. Typically, the higher your score, the lower your interest rates will be.

If your credit score is on the lower side, don’t lose hope. There are practical steps you can take to improve it before you apply for a mortgage loan.

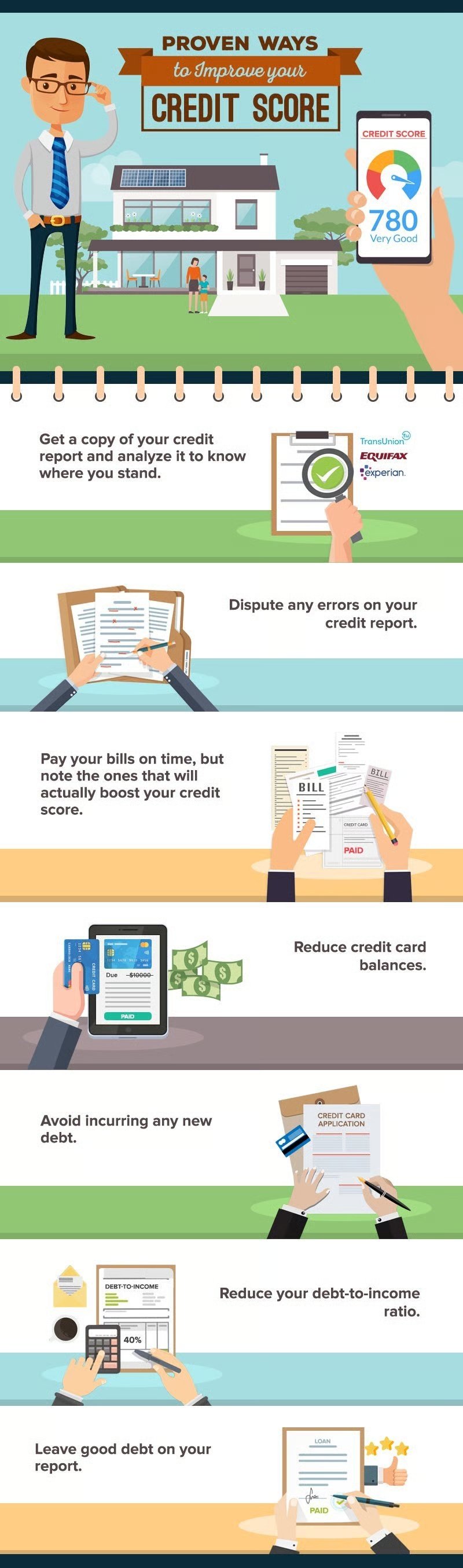

Step 1: Know Where You Stand

When applying for a mortgage loan, the first thing you should do is determine your credit standing.

Request a copy of your credit report from the three major reporting agencies:

Having all three reports allows you to perform an in-depth comparison since some creditors only report to one or two agencies. You can also calculate your average score, which is often what mortgage lenders use to determine your qualification.

Ideally, lenders should find a solid credit history, steady income, and proof of a down payment. While the process can feel daunting, you’re not alone—and your case isn’t hopeless. Once you’ve analyzed your credit report, you can work on improving problem areas to qualify for the best possible mortgage.

Step 2: Dispute Errors on Your Credit Report

It’s not unusual for credit reports to contain errors—such as inaccurate, incomplete, outdated, or unverifiable items. These can hurt your mortgage application.

If you spot mistakes:

-

Gather supporting documents to prove your case.

-

Contact the reporting agency to request corrections or removals.

-

Follow the official dispute process promptly.

Step 3: Pay Bills on Time—Focus on the Right Ones

Paying bills on time is essential, but not all bills will boost your credit score equally.

According to credit.com, on-time payments for rent, utilities, cable, internet, and cell phone bills generally don’t increase your score. However, late payments for these can hurt it—especially if sent to collections.

The payments that directly impact your credit score include:

-

Credit card bills

-

Student loan payments

-

Mortgage payments

-

Car loan payments

Make sure these are paid on time if you want to improve your score.

Step 4: Reduce Credit Card Balances

Having small balances on multiple credit cards can lower your score. Your credit score is affected by how many cards carry balances, so:

-

Pay off nuisance balances on multiple cards.

-

Stick to one or two main cards for regular purchases.

This keeps your credit report cleaner and more appealing to lenders.

Step 5: Avoid Taking On New Debt

To show lenders you’re financially stable, avoid new debt until your mortgage is approved. Credit inquiries affect your score, so skip applying for new credit cards or financing large purchases while your mortgage application is pending.

Step 6: Lower Your Debt-to-Income Ratio

Your debt-to-income ratio (DTI) is the percentage of your monthly income used to pay debts.

-

Low DTI = majority of your income is free from debt obligations.

-

High DTI = large portion of your income is tied to fixed expenses like rent or car payments.

Aim for a total DTI of 40% or lower to improve your mortgage approval chances. Higher ratios may raise red flags for underwriters.

Step 7: Keep Good Debt on Your Report

Not all debt is bad—if it’s been managed well. A history of successfully paid-off loans (like a car loan) shows lenders you’re responsible with credit.

Don’t rush to remove records of good debt; they help strengthen your credit profile.

Bottom Line

Improving your credit score takes time, but with these targeted steps, you can increase your chances of securing a mortgage with favorable terms.